What is Revenue Recognition?

Written by Arnon Shimoni

✓ Expert

Last updated on:

Revenue recognition is the accounting principle that determines when a company records revenue in its financial statements, not just that it received cash. Under accrual accounting (the basis for US GAAP and IFRS), revenue is recognized when it is earned (the company has transferred a good or service to a customer), not when cash changes hands. The modern global standards that govern this are ASC 606 in the US and IFRS 15 internationally, both built around the same five-step model.

Field | Detail |

|---|---|

Also known as | Revenue recognition principle, the realization principle |

Governed by | |

Effective for | All entities reporting under GAAP or IFRS |

Underlying principle | Revenue is earned when control transfers, not when cash is collected |

Accounting basis required | Accrual accounting |

Core mechanism | Five-step model for contracts with customers |

Five common methods | Sales-basis, over-time (percentage-of-completion), installment, completed-contract, cost-recoverability |

Related liabilities | Deferred revenue (unearned), accrued revenue (earned but unbilled) |

Most affected industries | Software/SaaS, telecom, construction, media, professional services |

Why does revenue recognition exist?

Without rules for when to record revenue, two companies with identical contracts and identical cash flows could report wildly different revenue numbers in the same period. One could book a four-year contract as $6 million in year one. Another could spread it evenly over 48 months at $125,000 per month. Investors comparing the two would see one growing 4x faster than the other, even though the underlying economics are identical.

Revenue recognition rules exist to make financial statements comparable across companies, industries, and time periods. They sit at the intersection of two foundational accounting principles: the accrual principle (record economic events when they occur, not when cash moves) and the matching principle (record expenses in the same period as the revenue they helped generate).

The history of revenue recognition is a slow march toward more standardization. Before 2018, US GAAP had more than 100 industry-specific revenue rules (software, real estate, construction, telecom, healthcare, media each had their own). ASC 606 collapsed those into a single principles-based model, with IFRS 15 doing the same for the rest of the world. Today, the world has effectively one revenue recognition framework, applied with minor jurisdictional differences.

What is the revenue recognition principle?

The revenue recognition principle states that revenue should be recognized in the period in which it is earned, regardless of when cash is received. “Earned” has a specific definition under modern standards: revenue is earned when control of the promised good or service transfers to the customer.

Control means the customer has the ability to direct the use of the good or service and obtain substantially all of the remaining benefits from it. This is a deliberate shift from the older “earnings process” language used under legacy US GAAP. The old standard asked whether the seller had substantially completed what it was required to do. The new standard asks whether the customer has received what they paid for.

This shift matters most for industries where the cash payment timeline and the delivery timeline are very different. A SaaS company often collects an annual subscription upfront in cash but delivers the service over 12 months. A construction company collects payments on a milestone schedule but delivers a building over years. A consultancy may bill on net-60 terms but deliver the work in week 1. Revenue recognition rules align the income statement with the actual economic activity, not the cash flow.

What are the methods of revenue recognition?

Five methods cover most revenue arrangements. Under ASC 606 and IFRS 15, the choice of method is determined by analysis under the five-step model, not by free selection.

Sales-basis method. Revenue is recognized at the point of sale, when the good is delivered or the service is rendered. This applies to most retail transactions and product sales. The cash form (cash vs credit) does not affect timing.

Over-time method (formerly percentage-of-completion). Revenue is recognized as the entity satisfies the performance obligation over time. This applies when the customer simultaneously receives and consumes the benefit, the entity’s performance creates an asset the customer controls, or the entity’s work has no alternative use plus a right to payment. SaaS subscriptions, long-term construction contracts, and most professional services use this method.

Installment method. Revenue is recognized as each installment payment is received. Used historically for high-credit-risk sales (real estate, car sales with sub-prime financing). Less common today.

Completed-contract method. Revenue is recognized only when the entire contract and all performance obligations are fulfilled. Rare under modern standards because ASC 606 favors over-time recognition wherever the criteria are met.

Cost-recoverability method. Revenue is recognized only after all costs associated with the transaction have been recovered. Used for high-uncertainty arrangements (early-stage R&D contracts, distressed asset sales).

For most modern software and AI companies, the sales-basis and over-time methods cover 95%+ of arrangements. SaaS subscriptions recognize over time. One-time license sales recognize at a point in time. Professional services recognize over time. Hardware product sales recognize at a point in time.

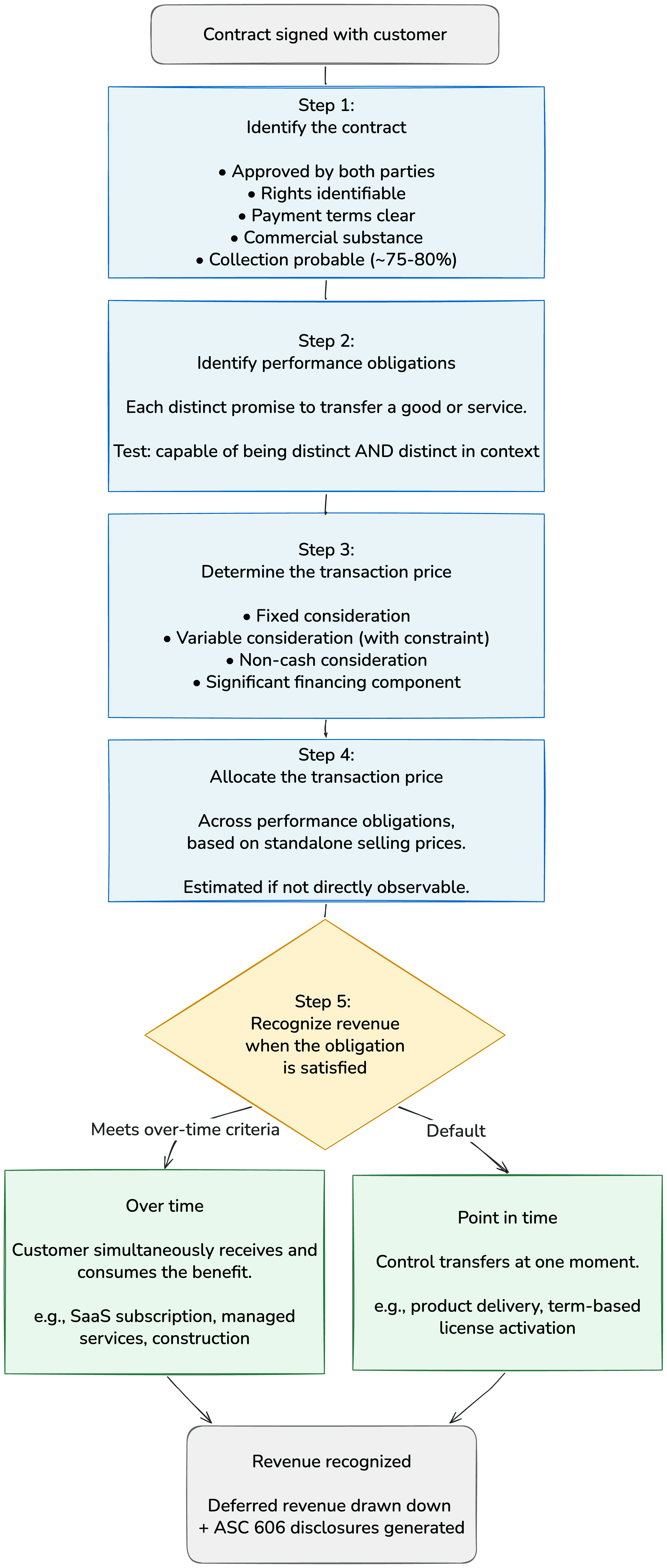

How is revenue recognition done today (ASC 606 and IFRS 15)?

Both standards apply the same five-step model to every revenue arrangement.

Identify the contract with the customer.

Identify the performance obligations (distinct promises) in the contract.

Determine the transaction price (fixed + variable consideration).

Allocate the transaction price across performance obligations using standalone selling prices.

Recognize revenue when (or as) each performance obligation is satisfied.

The output of the model is a recognition schedule for every performance obligation in every contract. A multi-element SaaS contract (subscription + implementation + training + support) often produces 3-4 separate recognition streams, each with its own timing.

For a complete walkthrough of the five-step model with examples and the IFRS 15 differences, see our ASC 606 pillar article.

Common revenue recognition scenarios

Revenue recognition looks different across business models. The same $1,000 of cash collected from a customer can produce very different income statement results depending on the underlying arrangement.

Annual SaaS subscription (paid upfront). $1,200 collected on January 1 for a 12-month subscription. Revenue is recognized at $100 per month over the year. At signing, $1,200 sits in deferred revenue. At year-end, deferred revenue is zero and recognized revenue is $1,200.

Monthly SaaS subscription. $100 charged each month for the service delivered that month. Revenue recognition matches cash collection. No deferred revenue.

Usage-based / metered service. $0 collected upfront. The customer is billed monthly based on consumption. Revenue is recognized as usage occurs and is metered, regardless of billing date. If usage exceeds billing, the difference sits in accrued revenue (a receivable that hasn’t been invoiced).

One-time perpetual license. $50,000 paid for a perpetual software license, delivered on signing. Revenue is recognized at a point in time (the date access is granted), assuming the license grants right-to-use rather than right-to-access.

Multi-year B2B contract with milestones. $1 million contract for a 3-year implementation with 5 milestones. Revenue is recognized as each milestone is satisfied, with the transaction price allocated based on standalone selling prices.

Hardware + subscription bundle. A $500 device paired with a 24-month $50/month service. Under ASC 606, the device and the service are distinct performance obligations. The transaction price is allocated across them based on standalone selling prices, often resulting in more revenue being recognized at device delivery than the customer’s invoice suggests.

Variable usage credits / pre-purchased credits. Customer pays $10,000 upfront for a pool of usage credits. Revenue is recognized as credits are consumed, not at the point of purchase. Unused credits at the end of the period stay in deferred revenue (or are released as breakage if the company has historical evidence that some credits will never be used).

What is variable consideration?

Variable consideration is any part of the transaction price that depends on a future event. Common examples: performance bonuses, refund rights, rebates, volume discounts, usage-based fees with caps or floors, and customer loyalty credits.

Under ASC 606 and IFRS 15, variable consideration is estimated up front and included in the transaction price, subject to a constraint: only the amount the entity is highly probable (not just probable) not to reverse can be recognized. This means companies have to forecast their refunds, rebates, and bonuses at contract signing rather than waiting for them to crystallize.

The constraint is the practical brake on aggressive revenue recognition. Without it, a company could promise a 10% volume rebate, estimate that nobody will hit the threshold, and recognize the full price up front. With it, the company has to recognize a conservative estimate and true up later.

What’s the difference between deferred revenue and accrued revenue?

Two opposite sides of the timing gap between cash and recognition.

Deferred revenue (unearned revenue). Cash collected before the service has been delivered. Sits as a liability on the balance sheet until the performance obligation is satisfied. SaaS companies that bill annually accumulate large deferred revenue balances.

Accrued revenue (unbilled receivable). Service delivered before the customer has been billed. Sits as an asset on the balance sheet until invoiced. Usage-based pricing models often accumulate accrued revenue between metering and the monthly invoice cycle.

Both are normal under accrual accounting. Together they capture the difference between what the income statement shows (recognized revenue) and what the cash flow statement shows (cash collected).

Revenue recognition by industry

The five-step model is uniform, but industry application varies.

SaaS and software. Subscriptions recognize over time. Term-based licenses recognize at a point in time. Set-up and activation fees are typically allocated across the subscription period. Customer loyalty programs and referral credits are evaluated as separate performance obligations. Usage-based and hybrid pricing arrangements use variable consideration estimation.

Telecom. Bundled handset-plus-service contracts are split into distinct performance obligations, with transaction price allocated across them based on standalone selling prices.

Construction and engineering. Most contracts qualify for over-time recognition because the customer either controls the work-in-progress or the work has no alternative use. Output methods (units completed, milestones) and input methods (cost-to-cost) are both used.

Media and publishing. Subscriptions and distribution licenses follow the over-time / point-in-time analysis. Advertising contracts depend on whether ad spots are distinct.

Healthcare. Variable consideration estimation dominates, with significant judgment around third-party payor reimbursement rates.

Retail. Point-of-sale transactions are mostly sales-basis. Gift cards, loyalty programs, and warranties require ASC 606 analysis.

How Solvimon supports revenue recognition natively

Solvimon’s Revenue primitive runs the five-step model automatically against every contract in the system. Each step maps to a specific primitive in the platform:

Contracts and modifications live in Subscriptions and Subscription Schedules. Renewals, mid-term changes, and amendments are first-class objects with full audit history.

Performance obligations are derived from Catalog (products, plans, add-ons) and Entitlements (features and access grants). Each distinct promise in a contract is tracked as its own object with its own recognition treatment.

Transaction price combines fixed pricing from the Catalog with variable consideration tracked through Metering (usage events) and Pricing Groups (rebates, performance bonuses, multi-tier discounts). Variable consideration constraints are configurable per the standard.

Allocation uses standalone selling prices stored on the Catalog object, with automatic application of the allocation algorithm across performance obligations.

Recognition is posted to the Revenue ledger on every billing cycle. Deferred revenue is drawn down as obligations are satisfied. Accrued revenue is captured when usage is metered ahead of billing. Both balances reconcile to the underlying contract and invoice data at the line-item level.

The platform produces ASC 606 disclosures, IFRS 15 disclosures, and a parallel ledger for jurisdictions that need both. Auditors get an audit-ready trail from cash receipt to recognized revenue without reconciliation across systems.

Related terms

Deferred revenue (unearned revenue)

Frequently Asked Questions

What is the revenue recognition principle in simple terms?

Revenue should be recorded in the period it’s earned, not the period the cash is collected. If a customer pays you $1,200 in January for a 12-month service, you recognize $100 of revenue each month, not $1,200 in January.

When is revenue recognized under ASC 606?

Revenue is recognized when (or as) a performance obligation is satisfied, meaning when control of the good or service transfers to the customer. This can be over time (SaaS, services, construction) or at a point in time (product delivery, term licenses).

What’s the difference between revenue recognition and cash accounting?

Cash accounting records revenue when cash is received. Revenue recognition under accrual accounting records revenue when the service is delivered or the good is transferred, regardless of when cash is received. US GAAP and IFRS both require accrual accounting for most companies.

What is the matching principle?

The matching principle requires expenses to be recorded in the same period as the revenue they helped generate. It’s the companion to the revenue recognition principle and ensures the income statement reflects the actual economics of a period.

What’s the difference between deferred revenue and accrued revenue?

Deferred revenue is cash collected before the service has been delivered (a liability). Accrued revenue is service delivered before the customer has been billed (an asset). They’re opposite sides of the same timing mismatch.

Does revenue recognition apply to private companies?

Yes. ASC 606 applies to all entities reporting under US GAAP, public or private. Private companies had an extra year to adopt (fiscal years after December 15, 2018).

Can I use cash-basis accounting and skip revenue recognition?

Pure cash-basis accounting is allowed for tax purposes for some small businesses but not for GAAP or IFRS financial reporting. Any company that produces audited financial statements applies revenue recognition.

How does revenue recognition apply to SaaS subscriptions?

SaaS subscriptions are recognized over time because the customer simultaneously receives and consumes the benefit. An annual subscription paid upfront is recognized in equal monthly increments (or based on usage if metered), with the upfront cash sitting in deferred revenue until earned.

How does revenue recognition apply to usage-based pricing?

Revenue is recognized as usage is metered and the corresponding service is delivered, regardless of when the customer is billed. Usage that’s been delivered but not yet billed sits in accrued revenue.

What is variable consideration?

Any part of the transaction price that depends on a future event: performance bonuses, refund rights, rebates, volume discounts, usage-based fees with caps. Under ASC 606, variable consideration is estimated up front and constrained to the amount highly probable not to reverse.

How does revenue recognition affect SaaS metrics like ARR?

Revenue recognition governs GAAP revenue (the income statement number). ARR is an operational metric that may not match GAAP revenue, especially when contracts include set-up fees, variable consideration, or front-loaded recognition (e.g., point-in-time license elements). Most SaaS companies report both with a reconciliation between them.

What changed in 2018 when ASC 606 took effect?

US GAAP moved from more than 100 industry-specific revenue rules to a single principles-based model. The biggest practical changes for SaaS: set-up fees, term licenses, multi-element arrangements, and customer loyalty programs all got re-evaluated. See our ASC 606 article for the full breakdown.

Solvimon’s Revenue primitive applies ASC 606 and IFRS 15 to every contract in the platform, from a single ledger.

Related

ASC 606 for usage-based and AI businesses. How the five-step model applies when revenue depends on usage.

Solvimon automated invoicing. Compliant invoices generated straight from billing data.

Revenue recognition for SaaS businesses. The basics of rev rec applied to subscription software.

Ready for billing v2?

Solvimon is monetization infrastructure for companies that have outgrown billing v1. One system, entire lifecycle, built by the team that did this at Adyen.