What is IFRS 15?

Written by Arnon Shimoni

✓ Expert

Last updated on:

Revenue recognition sounds like an accounting formality until you’re mid-deal and can’t agree with your auditor on whether you’ve “delivered” anything yet. IFRS 15, titled “Revenue from Contracts with Customers” is the international standard that resolves that question. Issued by the International Accounting Standards Board (IASB) and effective from January 2018, it replaced a patchwork of industry-specific guidance with a single framework covering nearly every contract a company signs. Its US equivalent, ASC 606, applies the same five-step model under slightly different terminology. The standards were developed jointly and are substantially converged.

The core principle is precise: recognize revenue in an amount that reflects the consideration you expect to receive in exchange for transferring goods or services to a customer. The standard doesn’t care what your contract says, what your billing system calculates, or when cash lands in your bank account. It cares about when control of something valuable passes to a customer.

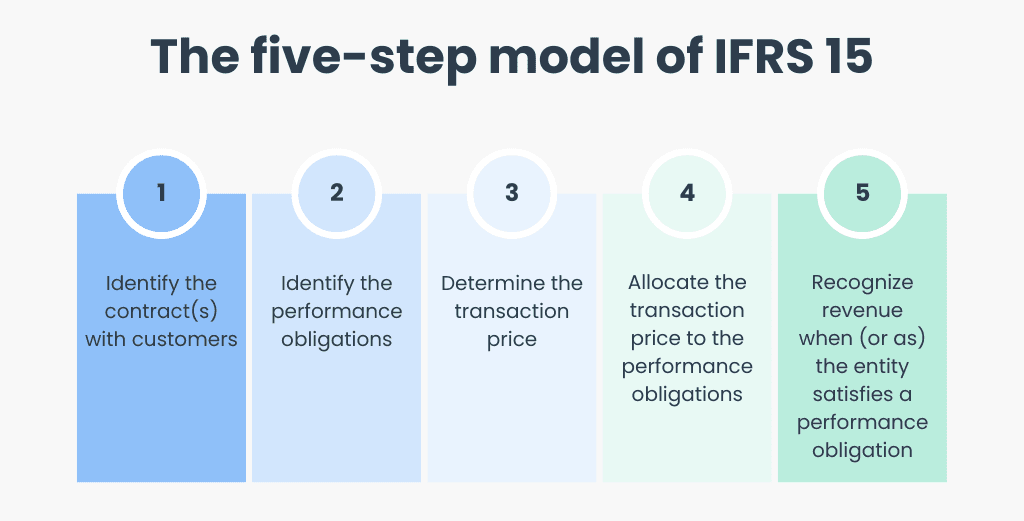

The Five-Step Model

IFRS 15 structures all revenue recognition decisions through five sequential steps. Every contract, regardless of industry or complexity, runs through this framework.

Five step model chart via Synder

Step 1: Identify the contract

A contract under IFRS 15 requires five conditions:

The parties have approved it (written, verbal, or implied by customary practice)

Rights to goods or services can be identified

Payment terms can be identified

The contract has commercial substance (i.e., it changes the risk, timing, or amount of future cash flows)

Collection of consideration is probable

That fifth condition trips up companies more than the others. If it’s unlikely you’ll actually get paid (say, a new customer with no credit history signing a large annual contract), you may not have a contract under IFRS 15 at all, even if you’ve signed paperwork. No contract means no revenue recognition, regardless of what was delivered.

Contract modifications are treated as either a new contract (if new distinct goods or services are added at their standalone selling price) or a modification of the existing contract (if not). Modifications that don’t qualify as new contracts require retrospective or prospective adjustment to previously recognized revenue, which creates real complexity for subscription businesses mid-term.

Contract combinations apply when multiple contracts entered into at or near the same time with the same customer are economically linked. In those cases, IFRS 15 may require treating them as a single contract for revenue recognition purposes. Read more about contract combinations in this KPMG IFRS 15 handbook.

Step 2: Identify performance obligations

A performance obligation is a promise to transfer a distinct good or service to a customer. “Distinct” has a specific meaning here: a good or service is distinct if the customer can benefit from it on its own, or together with resources they already have, and it’s separately identifiable from other promises in the contract.

For a SaaS company bundling software, implementation, and training into one contract, each component may or may not be a separate performance obligation depending on whether each is:

Capable of being distinct: Can the customer use this without the other elements?

Distinct within the contract: Is it separable from the other promises, or does it function as one integrated whole?

A software license that only has value after implementation is complete is likely a single combined performance obligation, not two separate ones. A software license that can be used immediately alongside third-party implementation is more likely distinct.

Getting this step wrong has downstream consequences: every subsequent step (transaction price, allocation, timing) depends on how many performance obligations you’ve identified.

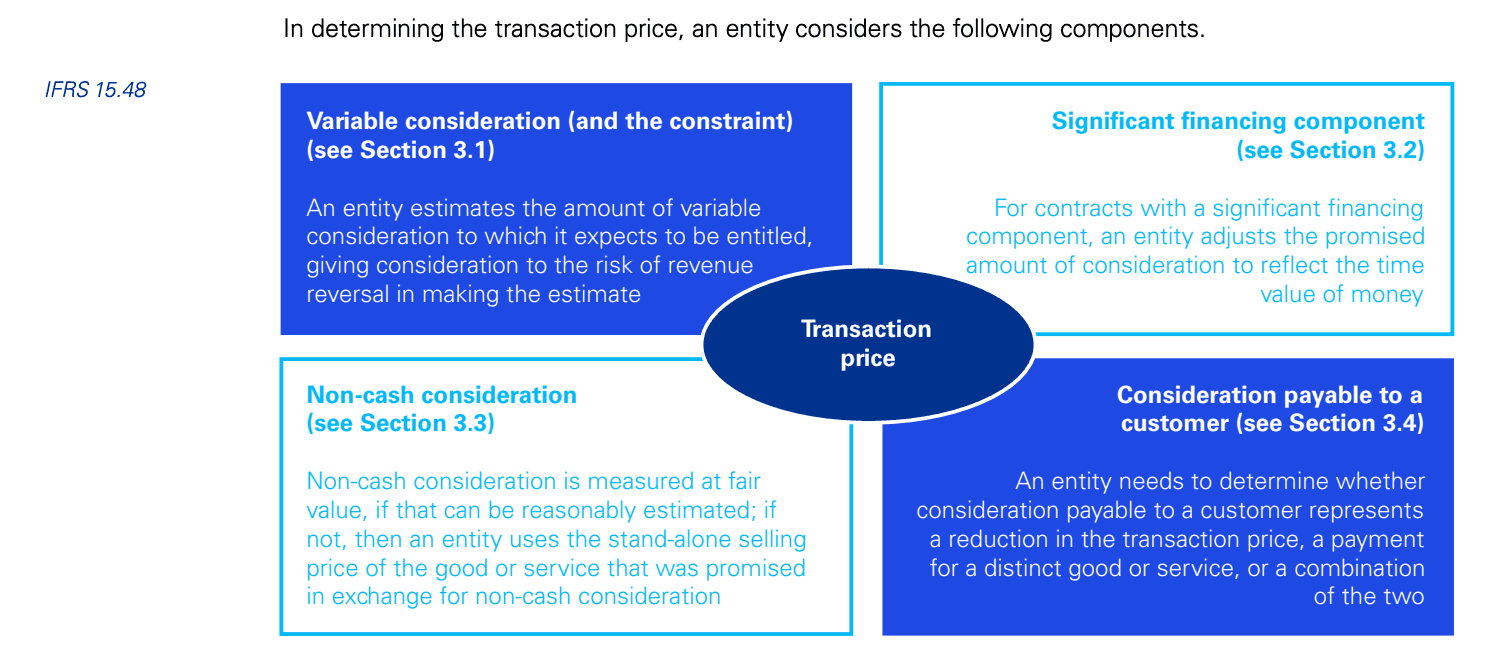

Step 3: Determine the transaction price

The transaction price is the amount you expect to be entitled to. Not the amount invoiced. Not the list price. The expected amount, accounting for:

Variable consideration covers discounts, rebates, refunds, credit memos, price concessions, incentives, performance bonuses, penalties, and contingent fees. IFRS 15 requires estimating variable consideration using either:

Expected value method: probability-weighted average of possible amounts

Most likely amount method: the single most likely outcome

Whichever method better predicts the amount must be used, and the estimate should only be included if it’s highly probable that a significant revenue reversal won’t occur when uncertainty resolves. This is the “constraint” on variable consideration. Companies can’t just recognize the full upside of a bonus they haven’t earned yet.

Chart via KPMG IFRS 15 handbook

Significant financing component: if the payment timing (either advance payment or deferred payment) gives one party a significant financing benefit, the transaction price must be adjusted to reflect the time value of money. The practical expedient: if the expected period between delivery and payment is less than one year, no adjustment is required.

Non-cash consideration: if a customer pays in shares, goods, or services rather than cash, the non-cash consideration is measured at fair value.

Consideration payable to a customer: if you pay the customer (rebates, coupons, payments for shelf space), these reduce the transaction price unless they’re for a distinct good or service received.

Step 4: Allocate the transaction price

Once you’ve identified your performance obligations and determined the transaction price, you need to allocate that price to each obligation in proportion to its standalone selling price (SSP).

Standalone selling price is what you’d charge if you sold that good or service separately. When that price is directly observable, use it. When it’s not, estimate it. IFRS 15 allows several estimation approaches:

Method | When to Use | How It Works |

|---|---|---|

Adjusted market assessment | Externally observable market prices exist | Estimate price the market would pay |

Expected cost plus margin | No observable price; cost structure known | Forecast costs plus appropriate margin |

Residual approach | SSP is highly variable or uncertain | Subtract known SSPs from total transaction price |

The residual approach can only be used if the price is genuinely variable. It can’t be used just because estimating SSP is inconvenient.

Allocation exceptions:

Discounts: If you have evidence that a discount applies to only a subset of performance obligations, the entire discount is allocated to that subset rather than spread proportionally.

Variable consideration: In some cases (commonly usage-based services), variable consideration can be allocated entirely to one performance obligation if it specifically relates to that obligation and the allocation faithfully depicts what you’re entitled to.

Step 5: Recognize revenue

Revenue is recognized when (or as) each performance obligation is satisfied. That happens when control transfers to the customer.

Over time: revenue is recognized progressively when any one of these criteria is met:

The customer simultaneously receives and consumes the benefits as the entity performs (e.g., a cleaning service)

The entity’s performance creates or enhances an asset the customer controls (e.g., building a structure on a customer’s land)

The entity’s performance creates an asset with no alternative use, and the entity has an enforceable right to payment for performance completed to date (e.g., a customized SaaS product built to spec)

When performance happens over time, revenue is recognized using a measure of progress toward completion: output methods (milestones, units delivered) or input methods (costs incurred, resources consumed).

At a point in time: if none of the over-time criteria are met, revenue is recognized at the point when control transfers. Indicators of control transfer include: the customer has a present obligation to pay, legal title has passed, physical possession has transferred, the customer has accepted the asset, and the customer has significant risks and rewards of ownership.

For software licenses, the distinction between over-time and point-in-time recognition is often one of the most contested judgments in an IFRS 15 audit. A license that grants a right to access software (as it exists over the period) is recognized over time. A license that grants a right to use software (as it exists at the point of grant) is recognized at a point in time.

IFRS 15 in Subscription and Usage-Based Businesses

For traditional subscription businesses, IFRS 15 is relatively straightforward: a subscription is a performance obligation satisfied over time, and revenue is recognized ratably across the subscription period. But the moment pricing gets complex, the standard’s edge cases multiply.

Usage-based revenue presents ongoing allocation and measurement challenges. If a contract includes a fixed fee plus usage-based fees, the fixed fee may be a distinct performance obligation recognized over time while the usage component falls under the variable consideration guidance. Alternatively, the usage component may be eligible for the “right to invoice” practical expedient: if what you invoice corresponds directly to the value delivered, you can recognize revenue in the amount invoiced.

Multi-element contracts are where IFRS 15 does its heaviest work for SaaS and AI companies. A deal bundling a platform license, professional services, and consumption-based API access involves potentially three distinct performance obligations, three separate SSP estimates, and three different recognition patterns: some over time, some at a point, some variable. Each element’s recognition is independent; completing the implementation doesn’t accelerate recognition of the license fee, and vice versa.

Contract modifications mid-subscription are common in enterprise SaaS and create some of the messiest accounting. Adding a new module partway through a contract year, restructuring pricing mid-term, or expanding to additional entities all require judgment on whether the modification creates a new contract or amends the existing one, which then determines whether historical recognized revenue needs to be adjusted.

Deferred revenue is a direct output of IFRS 15 in subscription businesses: cash collected before a performance obligation is satisfied creates a contract liability. A customer who pays annually upfront generates 11 months of deferred revenue on signing. Tracking and unwinding that balance accurately requires your billing system to feed revenue schedules, not just payment records, to your finance team.

IFRS 15 vs. ASC 606

Both standards were issued under a joint project and use the same five-step model. The conceptual differences are minor. The practical differences matter most for global companies applying both.

Dimension | IFRS 15 | ASC 606 |

|---|---|---|

Jurisdiction | International (IASB) | United States (FASB) |

Effective date | January 2018 | December 2017 (public) / 2018 (private) |

Principal vs. agent | Same framework, some interpretive differences | Same framework |

Licenses | Right to access vs. right to use distinction | Same, with more FASB technical guidance available |

Practical expedients | Available (right to invoice, financing component) | Same expedients, slightly different thresholds |

Industry guidance | Less prescriptive | More FASB ASC subtopics for specific industries |

Interpretive bodies | IASB; IFRIC issues interpretations | FASB; EITF issues guidance |

For a company reporting under both frameworks (common for US-listed foreign private issuers or companies with both IFRS and US GAAP reporting requirements), the standards are close enough that a single accounting policy memo often covers both, with jurisdiction-specific footnotes for areas of divergence.

Disclosure Requirements

IFRS 15 requires more disclosure than most companies anticipate. The standard mandates both quantitative and qualitative information across several categories:

Disaggregation of revenue: revenue must be broken out by the types, amounts, timing, and uncertainty that depict how economic factors affect the nature and amount of revenue. Most companies disaggregate by product line, geography, contract type (subscription vs. usage), or customer segment.

Contract balances: opening and closing balances of contract assets, contract liabilities (deferred revenue), and receivables, with an explanation of significant changes. For subscription businesses, this is essentially a deferred revenue waterfall.

Remaining performance obligations: the aggregate amount of transaction price allocated to performance obligations not yet satisfied, commonly called backlog. Companies with contracts over one year must disclose when they expect to recognize this revenue.

Significant judgments: any judgments that significantly affect the amount or timing of revenue, including how over-time vs. point-in-time was determined, the methods used to measure progress, how SSPs were estimated, and how variable consideration was constrained.

Assets recognized from costs to obtain or fulfill a contract: capitalized sales commissions (incremental costs to obtain a contract) and contract fulfillment costs must be disclosed with amortization policy and amounts recognized.

Common Challenges

Variable consideration constraint is underestimated. Companies often recognize the maximum possible variable consideration, then reverse it when targets aren’t hit. IFRS 15 is clear: you recognize variable consideration only to the extent it’s highly probable that a significant reversal won’t occur. Setting that threshold requires genuine forecasting, not optimism.

SSP estimation for bundled contracts is contentious. When you don’t sell elements separately, estimating standalone selling prices requires documented methodology. If your SSP estimates are inconsistent across similar contracts, auditors will ask why, and “we negotiated differently” is not a complete answer. The methodology needs to be applied consistently or the allocation of revenue between elements becomes arbitrary.

Over-time recognition requires defensible measures of progress. A 30% cost incurred doesn’t always equal 30% of value delivered. Using input-based measures (costs, hours) requires that inputs reliably reflect output. If your project is 90% budgeted but 30% complete due to early cost overruns, recognizing 90% of revenue is wrong. The measure of progress has to track performance, not cost.

Contract modifications trigger retrospective complexity. When a modification doesn’t qualify as a new contract, you may need to cumulative-catch-up or prospectively adjust revenue. For fast-moving SaaS companies with frequent mid-term upgrades, the volume of modifications can make this a significant operational burden if your billing system doesn’t track contract state changes.

Timing mismatches with billing create operational friction. Revenue recognized under IFRS 15 rarely aligns cleanly with invoicing schedules. Annual upfront billing creates large deferred revenue balances. Milestone-based billing creates contract assets (revenue earned but not yet invoiced). Finance teams need to reconcile these separately, which requires clean data from both the billing system and the revenue recognition layer.

FAQ

Q: Does IFRS 15 apply to all companies?

It applies to all entities that report under IFRS and have contracts with customers, with limited exceptions: lease contracts (covered by IFRS 16), insurance contracts (IFRS 17), financial instruments (IFRS 9), and non-monetary exchanges between entities in the same line of business. For most SaaS, AI, and technology companies operating internationally, IFRS 15 covers the full revenue picture.

Q: How does IFRS 15 handle SaaS subscriptions?

A standard SaaS subscription is typically a single performance obligation (access to software over the subscription period) recognized ratably over time. Complexity enters when the contract includes implementation, professional services, or usage-based components. Each element that is “distinct” under Step 2 becomes its own performance obligation with its own recognition pattern. Implementation services may be recognized over the implementation period; usage fees may be recognized as consumed. See ASC 606 for how the US framework handles the same question.

Q: What is a contract asset vs. a contract liability?

A contract asset arises when you’ve satisfied a performance obligation but don’t yet have an unconditional right to the consideration, for example completing Phase 1 of a project when payment is contingent on completing Phase 2. A contract liability (commonly called deferred revenue) arises when you’ve received payment before satisfying the performance obligation. Both appear on the balance sheet and must be tracked against each contract. See deferred revenue for the accounting treatment in detail.

Q: Can you recognize revenue from a contract that might be cancelled?

Only if the five criteria for contract existence are met, including that collection is probable. If a customer has a right to cancel without penalty, you need to assess whether a contract exists at all, or only exists for the period during which cancellation isn’t possible. For month-to-month subscriptions, this often means recognizing revenue only for the current month, even if you expect the customer to stay for three years.

Q: How does the “right to invoice” practical expedient work?

If you have a right to invoice that corresponds directly to the value delivered to the customer, you can recognize revenue in the amount you invoice rather than building a separate recognition model. This is useful for time-and-materials engagements and usage-based billing where the invoice accurately reflects the performance. The expedient only applies to over-time performance obligations and requires that the invoiced amount faithfully represents your entitlement for that period.

Q: What happens to capitalized sales commissions under IFRS 15?

Incremental costs of obtaining a contract, primarily sales commissions, must be capitalized and amortized over the period they generate economic benefit, which is typically the expected customer lifetime (not just the initial contract term). This has a material impact on income statements for high-growth SaaS companies with large sales teams. A practical expedient allows immediate expensing when the amortization period would be one year or less, which covers many short-cycle commission structures.

Related

Solvimon automated invoicing. Compliant invoices generated straight from billing data.

Deferred revenue. Cash collected before the revenue can be recognized.

ASC 606 for usage-based and AI businesses. How the five-step model applies when revenue depends on usage.

Ready for billing v2?

Solvimon is monetization infrastructure for companies that have outgrown billing v1. One system, entire lifecycle, built by the team that did this at Adyen.

AI Token Pricing

Entitlements

Seat-based Pricing

Usage-based Pricing

AI Factory

Token Factory

Neocloud Billing

GPUaaS Billing

Neocloud

Neocloud Metering

GPU-hour

Sovereign AI Billing

Credit-based pricing

Minimum Commit

Deferred Revenue

Usage Metering

Multi-currency Billing

E-invoicing

Hybrid Pricing Models

Revenue Backlog

Tiered Pricing

Stairstep Pricing

Sticky Stairstep Pricing

Tiered Usage-based Pricing

Revenue Leakage

Revenue Assurance

IFRS 15

ASC 606

France's E-Invoicing reform

Revenue Recognition

Prepaid vs Postpaid billing

Metering

Volume Commitments

Overage Charges

AI Agent Pricing

Outcome Based Pricing

Agentic Billing

Price Benchmarking

Freemium Model

Market Based Pricing

Odd-Even Pricing

Price Estimation

Marginal Cost Pricing

Quote to Cash

ACH

Subscription pause

Net Revenue Retention: How to Calculate It and What It Actually

PLG billing

Captive Product

Headless Monetization

Invoice

MRR & ARR

Subscription Management

Recurring Payments

Cost Plus Pricing

Dunning

Payment Gateway

Value Based Pricing

Consolidated Billing

Pricing Engine

Embedded Finance

Flat Rate Pricing

Yield Optimization

Grandfathering

Billing Engine

Predictive Pricing

AI-Led Growth

AISP

Advance Billing

Top Tiered Pricing

Region Based Pricing

High-Low Pricing

Lifecycle Pricing

Pay What You Want Pricing

Time Based Pricing

Contribution Margin-Based Pricing

Decoy Pricing

Dual Pricing

Loss Leader Pricing

Omnichannel Pricing

Revenue Optimization

Sales Enablement

Sales Optimization

Volume Discounts

Margin Management

Sales Prediction Analysis

Pricing Analytics

Intelligent Pricing

Margin Pricing

Price Configuration

Customer Profitability

Discount Management

Dynamic Pricing Optimization

Enterprise Resource Planning (ERP)

Guided Sales

Margin Leakage

Smart Metering

Quoting

CPQ

Self Billing

Revenue Forecasting

Revenue Analytics

Total Contract Value

Pricing Bundles

Penetration Pricing

Dynamic Pricing

Price Elasticity

Feature-Based Pricing

Transaction Monitoring

Minimum Invoice

SaaS Billing

Billing Cycle

Payment Processing

Multi-entity Billing

Ramp Up Periods

Proration

PISP

PSP

Why Solvimon

Helping businesses reach the next level

The Solvimon platform is extremely flexible allowing us to bill the most tailored enterprise deals automatically.

Ciaran O'Kane

Head of Finance

Solvimon is not only building the most flexible billing platform in the space but also a truly global platform.

Juan Pablo Ortega

CEO

I was skeptical if there was any solution out there that could relieve the team from an eternity of manual billing. Solvimon impressed me with their flexibility and user-friendliness.

János Mátyásfalvi

CFO

Working with Solvimon is a different experience than working with other vendors. Not only because of the product they offer, but also because of their very senior team that knows what they are talking about.

Steven Burgemeister

Product Lead, Billing