The payments layer is calling: Lovable's chance to build a true platform economy

Insights

Read time: 6 min

Kim Verkooij

✓ Expert opinion

I spent many years at Adyen watching companies decide what to own and what to outsource at the payments layer. The pattern is typically that companies that treat payments as plumbing, will stay as simple tools. However, companies that treat payments as infrastructure become platforms.

Last week Lovable shipped Lovable Payments with subscriptions and one-time purchases for every app built on the platform, integrated in minutes, with a third-party processor doing the heavy lifting underneath.

So while the builder picks the processor, Lovable handles the integration, and the monetization loop gets closed - and it's a pretty smart Q2 move.

It's also the first step of a much bigger opportunity, and I think Lovable is in a rare position to take it:

Shipping this now was the right call

Building a payments stack from scratch takes 18 to 24 months before you break even on the investment - and even then you can't really vibe-code it. It includes merchant onboarding, KYC, settlement, reconciliation, chargeback handling, fraud scoring, local payment methods per country and a lot more. It's not something you show in a demo, but it really does take intense engineering time.

At Adyen we used to say that the hardest part of payments isn't the first transaction but the millionth one, since that's when edge cases compound and the operational cost of every bip of failure becomes visible. It's quite a serious commitment at a moment when Lovable's real battleground is builder retention and app quality.

So they integrated and picked processors that work, shipped a clean UX, and let the builder community start monetizing today. Again, that's correct - you don't rebuild the foundation of a house you're still figuring out how to use.

What I find really great about this launch is what their next opportunity is:

What Lovable has in its hands right now

Lovable became the monetization entry point for a generation of builders which is a remarkable position.

Very few companies get to sit on top of a creator economy at this scale this early, and it has three assets that are interesting:

1. Margin headroom

Processing fees sit between 3% and 5% depending on the model. On low-ticket, high-volume AI subscriptions, which describes most apps built on Lovable, that's a meaningful slice of contribution margin. Every point Lovable brings in-house over time is permanent product funding.

2. A monetization dataset nobody else has

Whoever sees the payment sees the churn curve first because they know which pricing models convert.

As they watch which cohorts expand, Lovable is sitting on the monetization dataset of the vibe-coding economy. As Lovable moves closer to the transaction over time, that intelligence compounds into a real product advantage: better defaults, smarter pricing recommendations, benchmarks builders can't get anywhere else.

3. A product surface worth owning

The moment the billing and payments layer becomes part of Lovable's own product, entirely new things become possible. Custom pricing models tailored to AI apps. Credits that pool across users on the same team.

Hybrid plans with seats and usage in one invoice. Revenue sharing with builders that's native to the platform instead of reconciled in a spreadsheet - and while these aren't features the processors can't build, they're features the processors won't prioritize for Lovable's specific use case.

Owning the layer means Lovable gets to decide.

Yes - a strategic choice, not a technical one

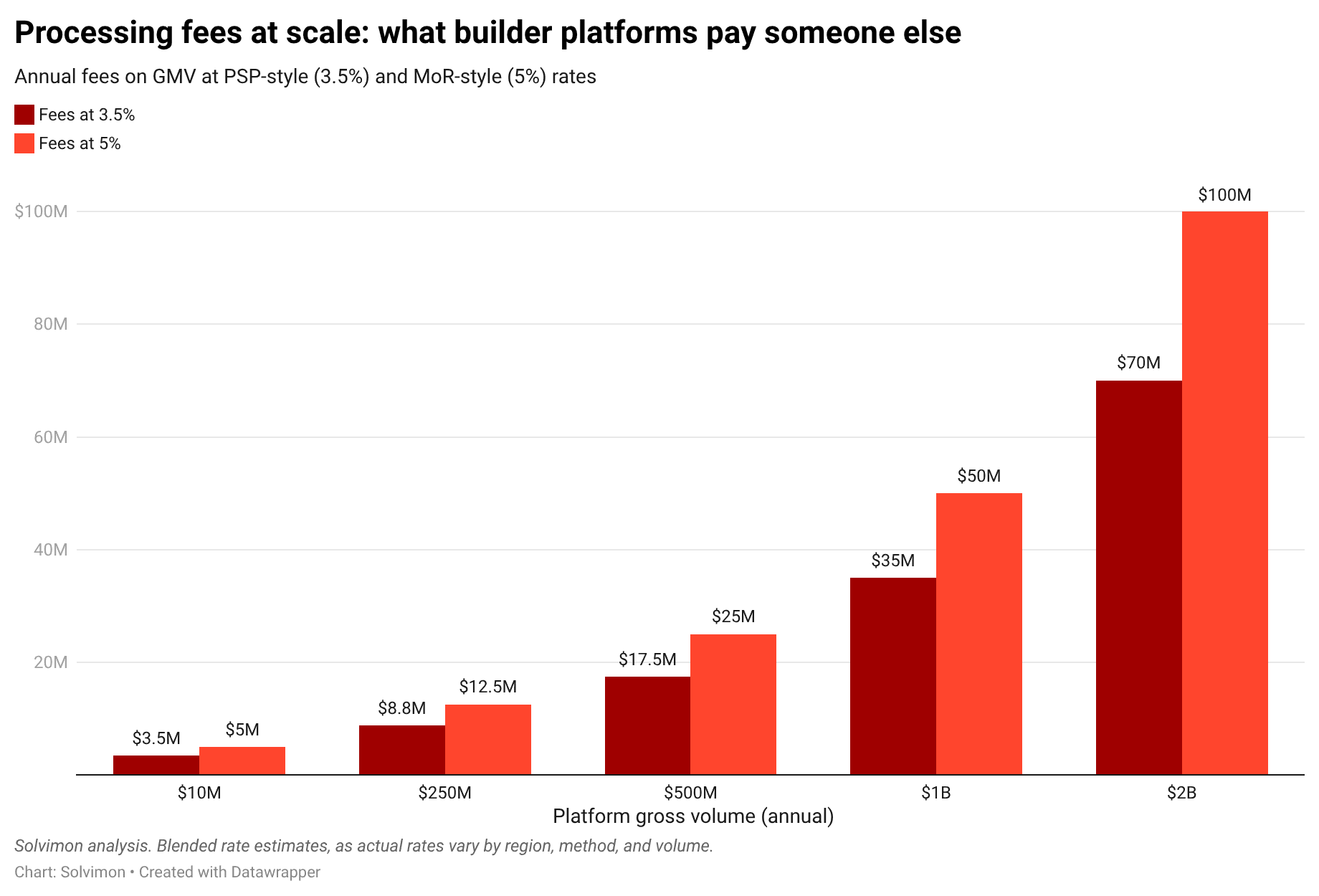

To make the opportunity concrete, here's what the economics look like across a range of GMV scenarios. The numbers aren't a projection of Lovable specifically. They're the shape any builder platform faces as it scales.

Annual GMV through platform | Fees at 3.5% | Fees at 5% | What that funds if kept in-house |

|---|---|---|---|

$100M | $3.5M | $5M | A 10-person billing team |

$250M | $8.75M | $12.5M | A billing team plus infrastructure build |

$500M | $17.5M | $25M | A Series B round, annually |

$1B | $35M | $50M | A Series C round, annually |

$2B | $70M | $100M | Break-even on an in-house PSP |

Assumptions: Blended processing rate of 3.5% (PSP-style pricing) to 5% (merchant-of-record-style pricing). Real-world rates vary by region, payment method, and chargeback profile. Excludes interchange-plus arrangements at high volume.

Somewhere in the low single-digit billions of GMV, the in-house payments operation pays for itself. Every dollar above that line is pure margin recovery that funds the product.

This is the math Shopify ran before they built Shop Pay. It's the math Uber ran before they built their own. It's the math every platform runs when it decides to graduate from tool to economy.

The three levels of owning payments

"Build your own payments" gets thrown around, but there are three levels, and they don't all require the same investment.

Level 1: Own the billing layer. Pricing logic, invoicing, entitlements, credit ledgers, revenue recognition. This is where most of the product differentiation lives, and it's where the processor has the least advantage over you. You can own this without touching the payments rail. Most platforms should start here.

Level 2: Own the payments orchestration. You still use processors underneath, but you route intelligently across different methods, different regions, and different risk profiles. You keep the customer relationship, the data, and the economics.

Level 3: Become a payment facilitator or merchant of record yourself. This is the Shopify Shop Pay move. Highest investment, highest return, only makes sense at scale.

Lovable doesn't need to jump to Level 3 tomorrow. The Q2 launch set them up to start at Level 1 whenever they're ready, and Level 2 follows naturally. That's a very strong position to be in.

A rare moment

Most companies have to choose between shipping monetization and owning it, but Lovable doesn't. They shipped first, which means they now have something better than a payments roadmap. They have a payments dataset. They can see exactly what their builders are selling, which models work, where the friction lives, and what the real unit economics look like before committing a single engineer to building the next layer.

That's the right way to sequence this. Ship to learn, then build to own.

Are you in a similar spot?

If you're running Lovable, or any of the other builder platforms approaching this decision (yes - that means Replit, Bolt, v0, Cursor), the question I'd put on the table isn't "should we build payments." It's:

At what GMV does owning more of the payments layer become a better investment than any other use of the same engineering dollars?

That number exists for every platform, but it'll be different. Once you know it, everything about the roadmap gets clearer.

Bottom line

Lovable just did the hard part. They shipped. The payments layer is now calling. The opportunity on the other side of this launch is the chance to convert a great product into a true platform economy, one where Lovable defines the monetization rules, keeps more of the margin, and owns the data that makes the next generation of builders successful.

I built billing at Adyen for eight years. I've watched this exact moment arrive for a lot of companies. The ones that answered the call became platforms. Lovable has everything it needs to do the same, and it'll be interesting to watch them do it!

Ready for billing v2?

Solvimon is monetization infrastructure for companies that have outgrown billing v1. One system, entire lifecycle, built by the team that did this at Adyen.